Removing Founder Dependency from Your GTM Before a Sale or Fundraise

- Roger M.

- Jun 19

- 7 min read

The acquirer’s diligence team asks one question that determines more about your valuation than any other: “What happens to pipeline if the founder steps back from sales?”

If the honest answer is “it drops by 40 to 60 percent,” the company has founder dependency. And founder dependency is the single largest valuation discount in B2B acquisitions. It is not priced as a small risk adjustment. It is priced as a structural deficiency that the acquirer must spend 12 to 18 months and significant capital to fix post-acquisition. That cost is deducted from the purchase price.

McKinsey’s Global Private Markets Report 2026 reports that 60 to 70 percent of PE-backed companies change their C-suite during ownership. The acquirer is not asking the founder dependency question out of curiosity. They are asking because they plan to operate the company without the founder — and they need to know whether the revenue engine survives that transition.

How do you reduce founder dependency before selling a company?

Reducing founder dependency is a systematic process of extracting what the founder knows and does, encoding it into documented systems, and proving that the team can execute those systems independently. It follows five steps over four to six months.

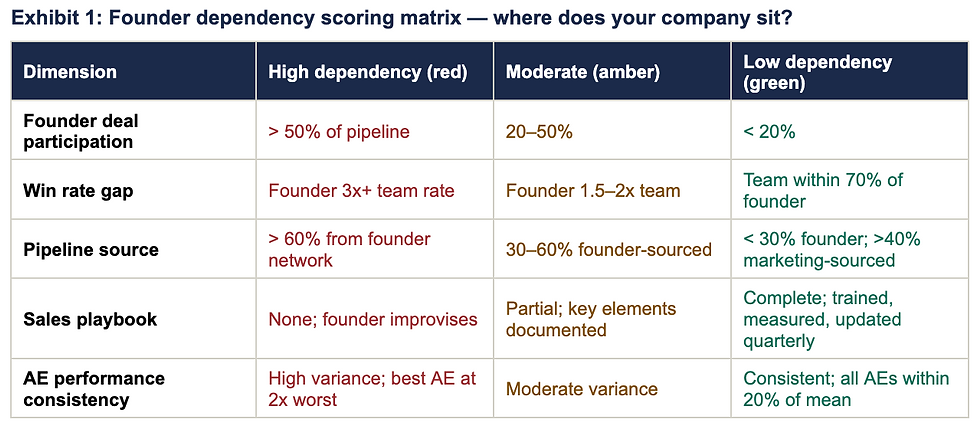

Step 1: Quantify the dependency. Measure founder deal participation as a percentage of total pipeline and closed-won revenue. Calculate founder versus team win rates. Identify which stages of the sales cycle require the founder (discovery, demo, negotiation, close). Map every pipeline source: how much originates from the founder’s personal network versus systematic demand generation? This baseline becomes the starting point and the metric the entire programme is measured against. Most founders overestimate their team’s independence. The data almost always reveals that founder involvement is higher than perceived — often because the founder joins calls “just to help” without registering it as deal participation. The honest baseline is the foundation of the entire transition.

Step 2: Extract the founder’s playbook. The founder’s effectiveness is not magic — it is pattern recognition built over years. Sit in on the founder’s next 15 to 20 sales calls. Record and transcribe every one. Identify the patterns: how do they open? Which pain points do they lead with? How do they handle pricing objections? What creates urgency? What do they say about competitors? Document every pattern into a structured playbook: discovery framework, value proposition structure, objection handler library, competitive positioning matrix, and closing sequence.

Step 3: Transfer the playbook to the team. The playbook is not a script. It is a decision framework. Train AEs against it through structured role-plays, call reviews, and coached live calls. The founder joins calls initially as co-pilot — not leading, but observing and coaching afterward. After each call, structured feedback compares what the AE did against the playbook. The milestone: at least two AEs must consistently achieve 70 percent of the founder’s historical win rate, on their own, executing the playbook.

Step 4: Build systematic demand generation. Founder-sourced pipeline typically comes from personal network, conference relationships, and inbound from the founder’s personal brand. None scale beyond the founder’s capacity. Replace these with systematic channels: content marketing against the validated ICP, paid acquisition with attribution tracking, ABM for highest-value accounts, and outbound sequences built on the documented playbook. The goal: marketing-sourced pipeline must exceed founder-sourced pipeline before the transaction. Companies with precise ICP targeting achieve 2.5 times higher conversion rates (Bain), making systematic demand gen more efficient than founder-led prospecting at scale.

The first 90 days of systematic demand gen will not match the founder’s personal pipeline volume. But by month six, the systematic channels should be generating more qualified pipeline at lower cost per opportunity than the founder’s network ever did — and they scale linearly with investment.

Step 5: Prove independence with data. Track founder deal participation monthly. The trajectory should show a clear decline: from 60 percent at baseline to below 20 percent by the end of the programme. Simultaneously, track team-sourced pipeline and win rates. The investor needs to see not just that the founder stepped back, but that the revenue engine performed at or near historical levels without the founder’s direct involvement. This proof is what converts a “founder-dependent” discount into a “GTM-independent” premium.

How do investors view founder-led sales?

Investors do not penalise founder-led sales at the early stage. At Series A, founder-led sales is expected — the founder is the best salesperson because they built the product and understand the customer better than anyone. The penalty begins when the company has raised Series B or later capital, has hired AEs, and the founder is still closing the majority of deals. At that point, founder-led sales is not a feature. It is a failure to build a system.

The investor’s concern is specific: founder dependency is concentration risk. In PE contexts, concentration risk is priced into the multiple. A company where one customer represents 30 percent of revenue receives a discount. A company where one person represents 60 percent of pipeline receives the same treatment. The risk is identical — if that person or customer leaves, the revenue degrades.

McKinsey’s data quantifies the context: over 16,000 companies have been held more than four years, representing 52 percent of total buyout inventory. Apollo describes “compelled sellers.” When these companies go to market, acquirers can afford to be selective. The companies with founder-independent GTM engines will command premium multiples. The ones where the founder is the GTM engine will compete on price.

The valuation maths is straightforward. A company at $20M ARR with founder dependency scores in the red zone on three or more dimensions will typically face a 1 to 3 multiple point discount. At 12x baseline, that means trading at 9x to 11x instead — a $20M to $60M gap in enterprise value. Conversely, a company that demonstrates clear founder independence — team win rates within 70 percent of founder, marketing-sourced ARR above 40 percent, documented playbooks, consistent AE performance — earns a premium that reflects the reduced execution risk. The cost of building this independence is measured in the low hundreds of thousands. The valuation impact is measured in the tens of millions.

Partners Capital’s Insights 2026 adds the fundraising dimension. With global VC fundraising at its lowest since 2017 and capital concentrating around top funds, investors are increasingly discriminating on GTM maturity. A Series B or C pitch where the founder admits to closing 60 percent of deals raises an immediate red flag: can this company scale to justify the valuation I’m underwriting? A pitch where the founder demonstrates systematic reduction in their deal involvement — backed by data showing team performance converging with founder performance — answers the question before it is asked.

How do you build a sales process that doesn’t depend on the founder?

The sales process that survives founder departure has four properties, each of which must be documented, trained, and measured.

The transition timeline is four to six months. Phase 1 (months 1–2): extract and document the playbook; validate ICP from closed-won data; build attribution infrastructure. Phase 2 (months 2–4): train AEs against the playbook; founder shifts to co-pilot role; systematic demand gen activated. Phase 3 (months 4–6): founder reduces to strategic accounts only; team pipeline exceeds founder pipeline; independence metrics hit target thresholds.

The most critical milestone is the handoff point at the end of Phase 2, when the founder moves from active seller to observer-coach. This is psychologically the hardest moment for most founders. They have spent years being the best salesperson in the company. Watching an AE stumble through a pitch they could close in their sleep requires discipline that feels counterproductive. But the data consistently shows that teams that are given autonomy to execute the playbook — with coaching support but without founder takeover — reach independence faster than teams where the founder keeps stepping in. Every time the founder rescues a deal, it resets the AE’s learning curve and reinforces the dependency the programme is designed to eliminate.

The most common mistake is rushing the transition. Founders who withdraw from sales before the playbook is documented and AEs are validated see win rates collapse and pipeline stall. The instinct is to jump back in — which resets the dependency clock. Discipline requires trusting the system and giving the team time to achieve independence, even through an initial dip in conversion rates. The dip is normal. It typically lasts four to eight weeks. Teams that push through it emerge with stable, independent performance. Teams where the founder re-engages never get through it.

A fractional CMO with experience managing this transition across multiple companies brings two critical capabilities: the framework for extracting and documenting the founder’s playbook (which is a structured analytical process, not a casual conversation), and the emotional distance to maintain the transition plan when the founder’s instinct says to re-engage. The best fractional CMOs have seen the dip, know it is temporary, and can present the data that proves the system is working even when the numbers temporarily soften.

For companies approaching an exit or fundraise, founder dependency removal is the single highest-leverage intervention available. A $168K to $322K investment over 18 months (the total cost of a fractional CMO engagement including tech stack) that eliminates founder dependency and adds 1 to 3 multiple points on a $20M ARR company produces $20M to $60M in enterprise value. No other pre-exit investment offers comparable returns. The only question is whether you begin the process early enough to have the data that proves independence by the time the transaction arrives.

→ Book a founder dependency audit: rogemabag.com/revenue-diagnostic

A 30-minute session that scores your company on the five dependency dimensions, quantifies the valuation impact, and maps the four-to-six-month transition plan. No pitch. Just the diagnostic.

Sources: McKinsey & Company, Global Private Markets Report 2026; Partners Capital, Insights 2026; Apollo PE Outlook 2026; Bain & Company; SaaS GTM benchmarks 2025–26.

Comments